The $89 Million Bug: What Apple and Goldman Sachs Got Wrong About AI in Finance

I was sitting in my home office on a Tuesday evening last October when the CFPB press release hit my feed. Apple and Goldman Sachs, ordered to pay over $89 million for systemic failures in how they handled Apple Card disputes. I read the consent order twice. Then I read it a third time, because I couldn't believe what I was seeing.

The core failure wasn't some exotic financial engineering gone wrong. It wasn't a rogue algorithm making discriminatory lending decisions. It was a button. A secondary form in the Apple Wallet app that, when left incomplete by consumers, caused their billing disputes to vanish into a digital void. Tens of thousands of people reported unauthorized charges, and the system just... ate them. No investigation. No acknowledgment. No resolution. The consumers were left holding the bill.

I build AI systems for a living. My company, Veriprajna, focuses on what we call deep AI — neurosymbolic architectures that combine the flexibility of large language models with the mathematical rigor of formal verification. When I read that consent order, I didn't feel vindicated. I felt sick. Because everything that went wrong with the Apple Card was preventable. Not with better testing. Not with more engineers. With a fundamentally different way of thinking about how AI systems should be built for regulated industries.

What Actually Happened to Your Apple Card Dispute?

Let me walk you through the failure, because the details matter more than the headline number.

Apple and Goldman Sachs signed their partnership agreement in 2017. Apple would own the consumer experience — the sleek Wallet interface, the messaging system, the whole front end. Goldman Sachs would be the bank behind the curtain, issuing credit, processing transactions, and investigating disputes when things went wrong.

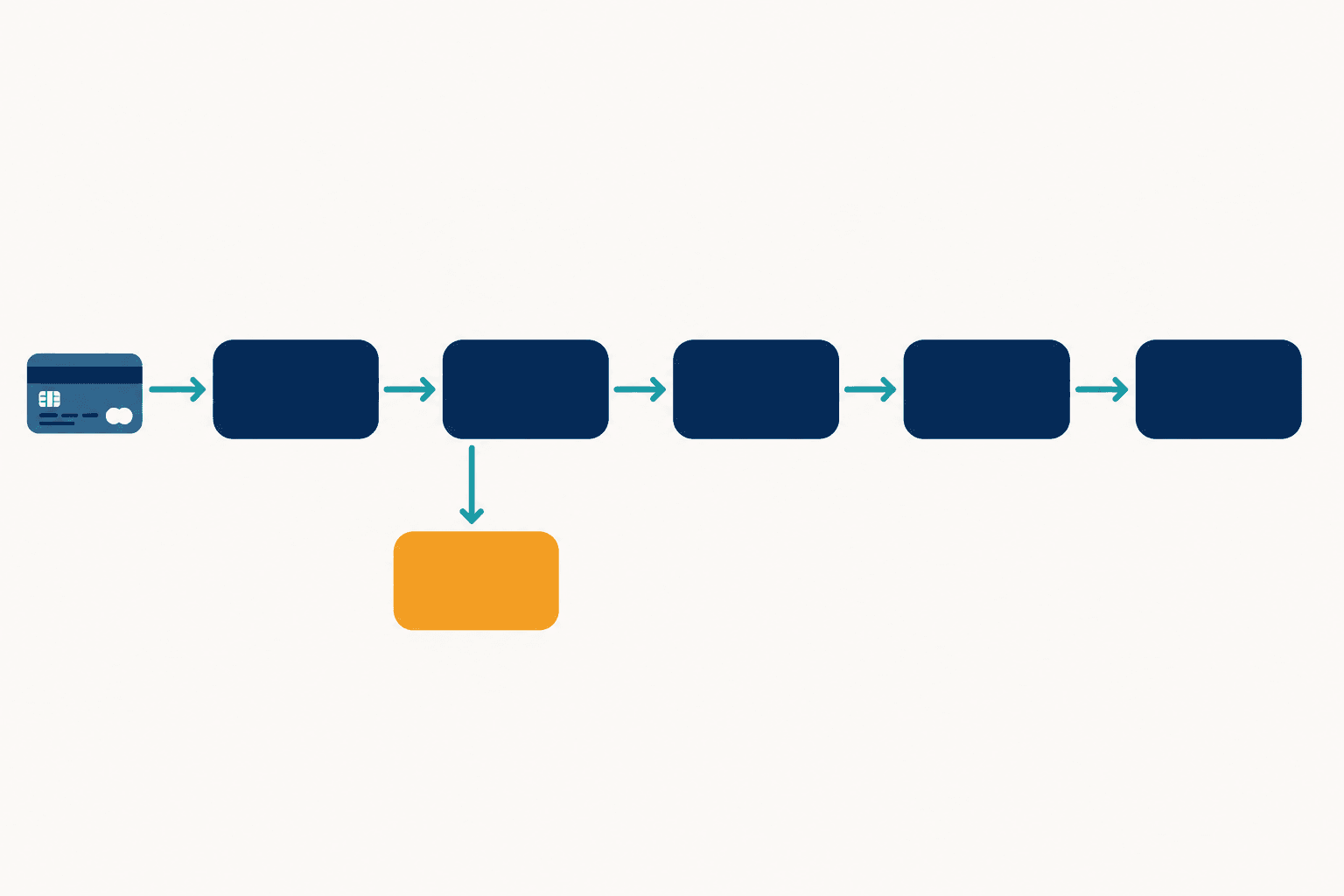

In June 2020, Apple pushed an update to the "Report an Issue" workflow. Before the update, you'd tap a suspicious transaction, hit "Report an Issue," and get routed to a Messages-based chat with Goldman Sachs. Straightforward. After the update, Apple added a secondary form — an extra step consumers were supposed to complete after their initial message.

Here's where it broke: when people submitted their dispute through Messages but didn't finish the secondary form, the system treated the dispute as incomplete. It never transmitted the complaint to Goldman Sachs. From a regulatory standpoint, many of these messages qualified as valid Billing Error Notices under the Truth in Lending Act. Legally, they should have triggered an investigation within specific timeframes. Instead, they disappeared.

Tens of thousands of legally valid consumer disputes were swallowed by a state machine that nobody had formally verified.

I remember reading that detail and thinking about every conversation I've had with financial services executives who tell me their systems are "battle-tested." Battle-tested against what? Against the specific scenario where a UI change introduces a dead state in a distributed workflow? That's not the kind of thing you catch with unit tests and QA sprints.

The $25 Million Clause That Broke Everything

There's a detail buried in the consent order that I keep coming back to. Apple's contract with Goldman Sachs included a provision for $25 million in liquidated damages for every 90-day delay Goldman caused in launching the Apple Card.

Twenty-five million dollars. Per quarter. For being late.

I've been in rooms where commercial pressure warps engineering decisions. I've watched teams ship things they knew weren't ready because the cost of delay felt more concrete than the cost of failure. But I've never seen the incentive structure spelled out this explicitly. Goldman Sachs was essentially fined in advance for being cautious.

The Apple Card went live on August 20, 2019. Internal teams at Goldman had flagged concerns about the system's readiness. The message queues between the Wallet app and Goldman's back-end were undertested. The synchronization protocols were fragile. But the math was simple: ship now and fix later, or pay $25 million and fix first.

They shipped. And for over a year, the system ran with a hole in it that nobody could see from the outside.

I think about this when people ask me why Veriprajna insists on formal verification before deployment. "Isn't that slow?" they ask. "Can't you just monitor in production and catch issues?" Sure. You can also drive without brakes and plan to steer around obstacles. It works until it doesn't. And when it doesn't work in financial services, real people get hurt.

Why Didn't Anyone Catch This?

This is the question that haunts me. Two of the most technologically sophisticated companies on the planet — Apple, with its legendary engineering culture, and Goldman Sachs, with its quantitative firepower — and neither one noticed that thousands of disputes were falling into a black hole?

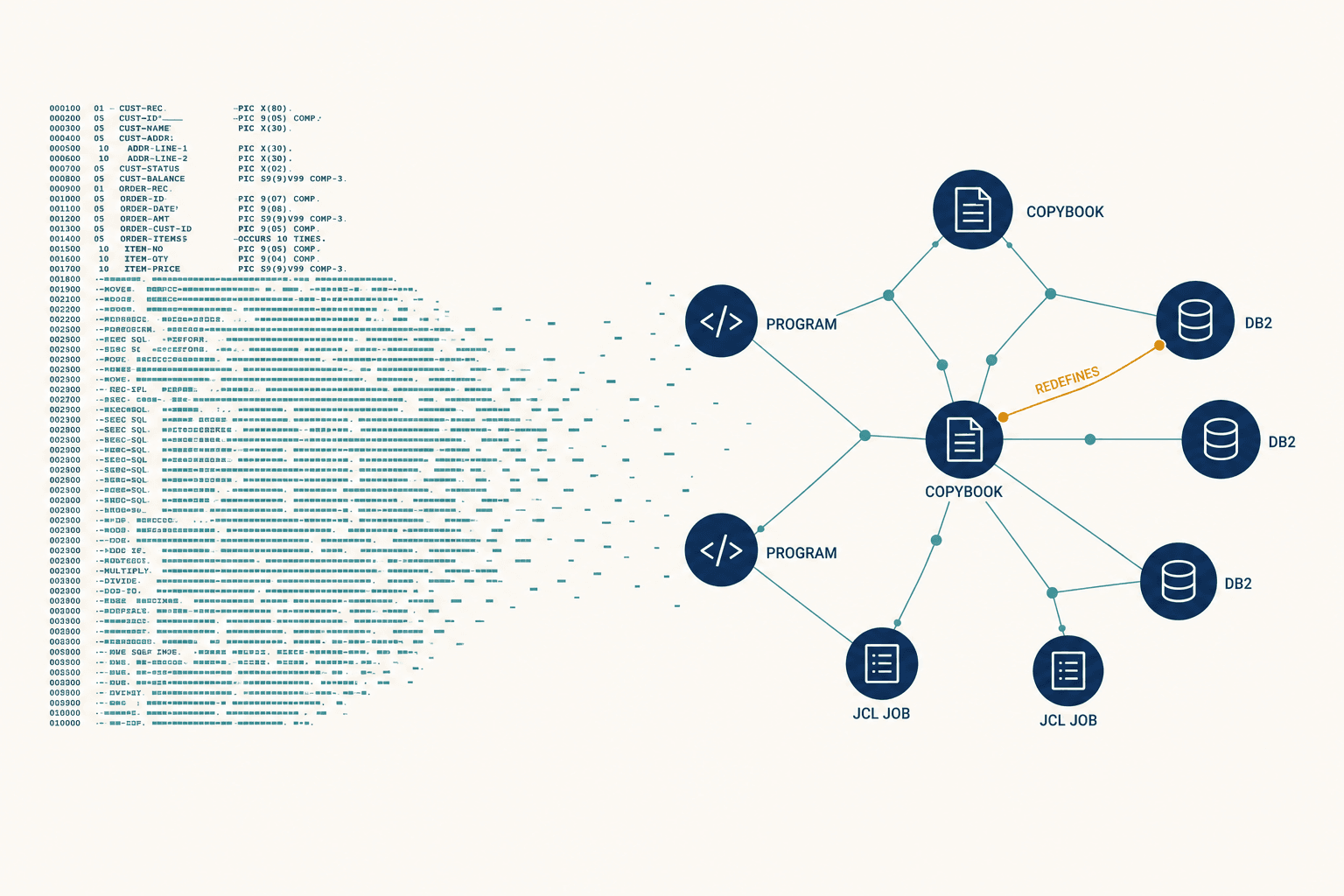

The answer, I think, is architectural. The system was designed as a relay: Apple handles the front end, Goldman handles the back end, and messages flow between them. But nobody owned the space between the two systems. Nobody had a formal model of what should happen when a dispute entered state A ("message submitted") but never reached state B ("form completed"). In a well-designed state machine, that's a transition you explicitly account for. In the Apple Card system, it was a gap that nobody specified, so nobody monitored.

I had a late night about a year ago — my team and I were building a compliance workflow for a client, and one of our engineers, Priya, flagged something similar. She'd been modeling the state transitions for a document review process and found a path where a submission could get stuck in a "pending enrichment" state indefinitely if a third-party API timed out. It wasn't a bug in the code. The code did exactly what it was told. It was a bug in the design — a state that the specification didn't account for.

We caught it because we use formal verification tools — specifically, we model workflows as state machines and run them through SMT solvers that exhaustively check every possible path. The solver found Priya's dead state in seconds. In the Apple Card system, that dead state ran in production for months.

The Apple Card failure wasn't a bug in the code. The code did exactly what it was told. It was a bug in the design — a state that nobody specified, so nobody monitored.

Why Can't You Just Use GPT for This?

I get this question constantly. An investor said it to me almost verbatim during a pitch meeting: "Why can't you just fine-tune GPT-4 on TILA regulations and have it handle disputes?"

I took a breath. Then I asked him: "If GPT-4 tells a consumer their dispute has been resolved, but it actually hasn't been transmitted to the bank, who's liable?"

He didn't have an answer. Neither does anyone else, because the question exposes the fundamental problem with what I call the "mega-prompt" approach to AI in regulated industries. You take a large language model, stuff the relevant regulations into its context window, and hope it handles everything correctly. No governance layer. No formal verification. No mathematical guarantee that the system's outputs are consistent with the law.

In the Apple Card case, the failure was a logic error in a distributed state machine. An LLM wrapper wouldn't have fixed this — it might have made it worse. Imagine an LLM confidently telling a consumer "Your dispute has been submitted and is being investigated" when, in reality, the dispute never left Apple's servers. That's not a hypothetical. That's what hallucination looks like in a financial context, and it's terrifying.

The popular financial explainer sites and widely-shared content about AI in banking almost universally miss this distinction. They talk about AI "automating" compliance as if the hard part is reading the regulations. The hard part isn't reading them. The hard part is proving that your system follows them in every possible scenario, including scenarios you haven't thought of yet.

For a deeper look at how the Apple-Goldman failure maps to specific regulatory violations and architectural gaps, I wrote an interactive analysis that walks through the consent order in detail.

What "Provably Correct" Actually Means

When I say Veriprajna builds "provably correct" compliance systems, I don't mean "really well-tested." I mean mathematically proven. There's a difference, and it matters enormously.

Testing checks specific scenarios. You write a test that says "if a user submits a dispute and completes the form, verify it reaches Goldman Sachs." That test passes. Great. But you haven't tested the scenario where the user submits a dispute and doesn't complete the form. Or where they complete it but the network drops the packet. Or where two disputes arrive simultaneously and one overwrites the other.

Formal verification doesn't check scenarios. It checks properties. You define a property — "every submitted dispute must eventually reach an investigation state" — and a mathematical solver exhaustively proves that the property holds in every possible execution of the system. Every path. Every edge case. Every race condition. If there's a single counterexample, the solver finds it and shows you exactly how the system can fail.

We use tools like Imandra, which lets us build what's essentially a digital twin of the compliance logic. The twin runs alongside the production system, and if the production code ever attempts an action that deviates from the verified model — like dropping a dispute because of an incomplete UI step — the system catches it in real time.

This is the kind of approach that would have caught the Apple Card bug before a single consumer was affected. During the design phase, an SMT solver would have immediately identified that the "CompletedFormB" variable wasn't a mandatory field under TILA. The transmission logic required it, but the law didn't. That mismatch is a provable defect, and it would have been flagged before deployment.

The Architecture We Actually Build

I want to be specific about what a "deep AI" compliance system looks like in practice, because vague claims about "AI-powered compliance" are part of the problem.

Veriprajna uses a multi-agent architecture. Instead of one monolithic AI trying to do everything, we deploy specialized agents with defined roles and boundaries. Think of it less like hiring one genius and more like assembling a team where everyone has a specific job and a supervisor checking their work.

An Intake Agent handles the messy, human part — parsing natural language disputes. When someone writes "I never bought this coffee in Seattle; I was in London that day," the agent extracts the key entities: the transaction, the merchant, the date, the nature of the claim. This is where LLMs genuinely shine.

But then — and this is where we diverge from every wrapper-based approach I've seen — the extracted information passes to a symbolic Policy Engine that doesn't predict or guess. It evaluates the dispute against first-order logic encodings of federal law. Does this message contain enough information to constitute a valid Billing Error Notice under TILA? The engine doesn't estimate. It proves.

A Workflow Agent enforces the sequence of operations. A Verification Agent runs real-time mathematical checks. An Audit Agent logs every interaction in what we call a "glass box" — complete transparency for regulators.

And critically, a Sentinel Agent monitors for exactly the kind of dead state that killed the Apple Card system. If a dispute sits in "submitted but not transmitted" for more than a defined threshold, the Sentinel doesn't wait for a human to notice. It autonomously determines whether the existing information is sufficient to proceed, packages it, and transmits it through a verified channel.

In a system built for absolute compliance, the law — not the UI — determines whether a dispute is valid. If a consumer has told you about an unauthorized charge, the absence of a completed form is your problem, not theirs.

Why Timing Is a Legal Requirement, Not a Performance Metric

There's another dimension to this that most technical discussions miss entirely. In financial compliance, time is law. Regulation Z doesn't just say you have to investigate disputes. It says you have to acknowledge them within specific periods and resolve them within 60 days. Goldman Sachs was fined partly because they failed to send acknowledgment notices within these windows.

My team spent months developing what we call Symbolic Latency analysis — a way to mathematically prove that a distributed system will complete its work within a regulatory deadline under worst-case conditions. Not average conditions. Not "95th percentile." Worst case.

Traditional monitoring tells you if your system was slow. Symbolic Latency tells you if your system can be slow. If a change to the UI code increases the worst-case processing time beyond the 60-day regulatory window, the deployment gets automatically rejected. You don't find out after the fact. You find out before you ship.

I remember the argument we had internally about whether this level of rigor was necessary. One of my engineers — a brilliant guy who'd spent years at a major cloud provider — pushed back hard. "You're adding weeks to the deployment cycle for a scenario that might never happen," he said. I pointed to the Apple Card consent order. "It happened," I said. "To Apple. To Goldman Sachs. To tens of thousands of consumers who did nothing wrong."

He didn't argue after that.

For the full technical breakdown of our formal verification approach, including the Performal methodology for latency bounds, see our research paper.

"But This Would Take Too Long to Build"

People always push back on this point, and I understand why. The Apple Card launched in months. A formally verified compliance architecture takes 18 to 36 months for full optimization in a legacy-heavy environment. That feels like an eternity in a world where competitors are shipping weekly.

But let me reframe the math. Apple and Goldman Sachs spent years building and launching the Apple Card. Then they spent years dealing with the fallout — internal investigations, regulatory examinations, legal costs, reputational damage, and ultimately $89.8 million in penalties and consumer redress. The "fast" approach wasn't fast. It was front-loaded speed with back-loaded catastrophe.

Our phased deployment approach acknowledges reality. You can't rip out a bank's core systems. COBOL mainframes that have been running since the 1980s aren't going anywhere overnight. So we integrate in layers: audit the existing architecture, build an intelligent API gateway, run the AI system in shadow mode to validate the legacy system's outputs, and gradually shift decision authority as the formal proofs accumulate.

The first phase — assessment and formal modeling — takes 14 to 20 weeks. By the end of it, you have a mathematical model of your compliance logic that can catch the kind of dead-state bugs that plagued the Apple Card. That's not 36 months. That's less than five months to a fundamentally safer system.

The Moment That Changed How I Think About This

There's a specific moment I keep returning to. It was about eight months ago, and we were running a proof-of-concept for a financial services client. We'd modeled their dispute resolution workflow as a distributed state machine and were running the formal verification suite.

The solver found eleven dead states.

Eleven paths through the system where a consumer's complaint could get stuck with no resolution and no alert. The client's engineering team had been running this system for three years. They'd processed millions of transactions. They had monitoring dashboards, alerting systems, quarterly audits. And none of it had caught these eleven holes.

The room went quiet when I showed them the results. Their head of compliance — a woman who'd spent twenty years in banking regulation — looked at the screen and said, "How many consumers fell into those states?"

We didn't know. They didn't know either. That's the thing about dead states in distributed systems: if nobody's watching for them, they're invisible. The consumers affected might have called customer service, gotten a runaround, and eventually given up. Or they might still be paying for charges they never made.

That's what the Apple Card failure looks like from the inside. Not a dramatic explosion. A slow, silent accumulation of harm that nobody can see until a regulator forces open the black box.

What the Next Five Years Look Like

The CFPB action against Apple and Goldman Sachs isn't an isolated event. It's the beginning of a regulatory reckoning with how technology companies handle financial infrastructure. As banking becomes more embedded — in phones, in apps, in platforms that weren't originally designed as financial services — the gap between "works most of the time" and "provably works all of the time" becomes a liability measured in hundreds of millions of dollars.

I think about the objection I hear most often: "Isn't formal verification overkill for most financial systems?" And my answer has become simpler over time. The Apple Card is one of the most visible consumer financial products in the world, built by two companies with essentially unlimited engineering resources. If they couldn't catch a dead state in a dispute workflow through traditional testing and monitoring, what makes you think your system is different?

The industry is moving toward what I call Absolute Compliance — not compliance as a checkbox exercise, but compliance as an architectural property. A system where adherence to law isn't something you verify after the fact but something you prove before deployment. Where the gap between the UI and the regulation is bridged not by human vigilance but by mathematical certainty.

The era of "ship fast and fix later" is incompatible with the "move money and protect people" requirements of global finance. The Apple Card proved that. The question is whether the industry learns the lesson before or after the next $89 million fine.

We're building that future at Veriprajna. Not because it's easy — formal verification of distributed financial systems is genuinely hard, and anyone who tells you otherwise is selling something. But because the alternative is what we saw in October 2024: two of the world's most powerful companies, a broken button, and tens of thousands of people left holding the bill for charges they never made.

That's not a technology problem. It's an engineering ethics problem. And the solution isn't better monitoring or faster patches. It's building systems that are correct by construction — systems where the math guarantees that no consumer's dispute will ever vanish into a void.

The $89 million fine is already paid. The real cost is the trust that was broken. Rebuilding it requires more than promises. It requires proof.