What it catches, shown three ways

The demo walks a BLOCK, a PASS, and an escalation, all on synthetic positions. The screenshots below are real captures of the running app.

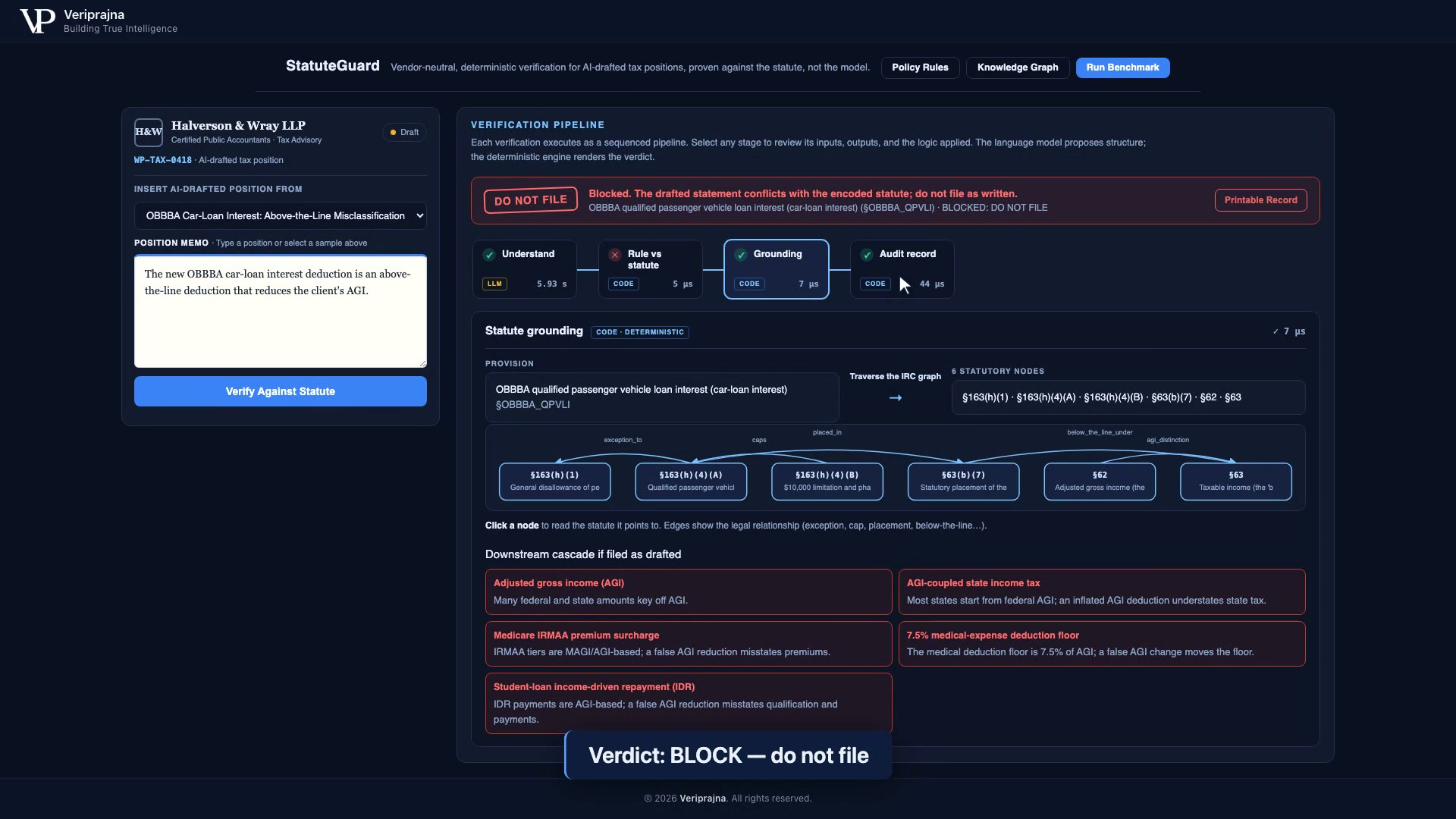

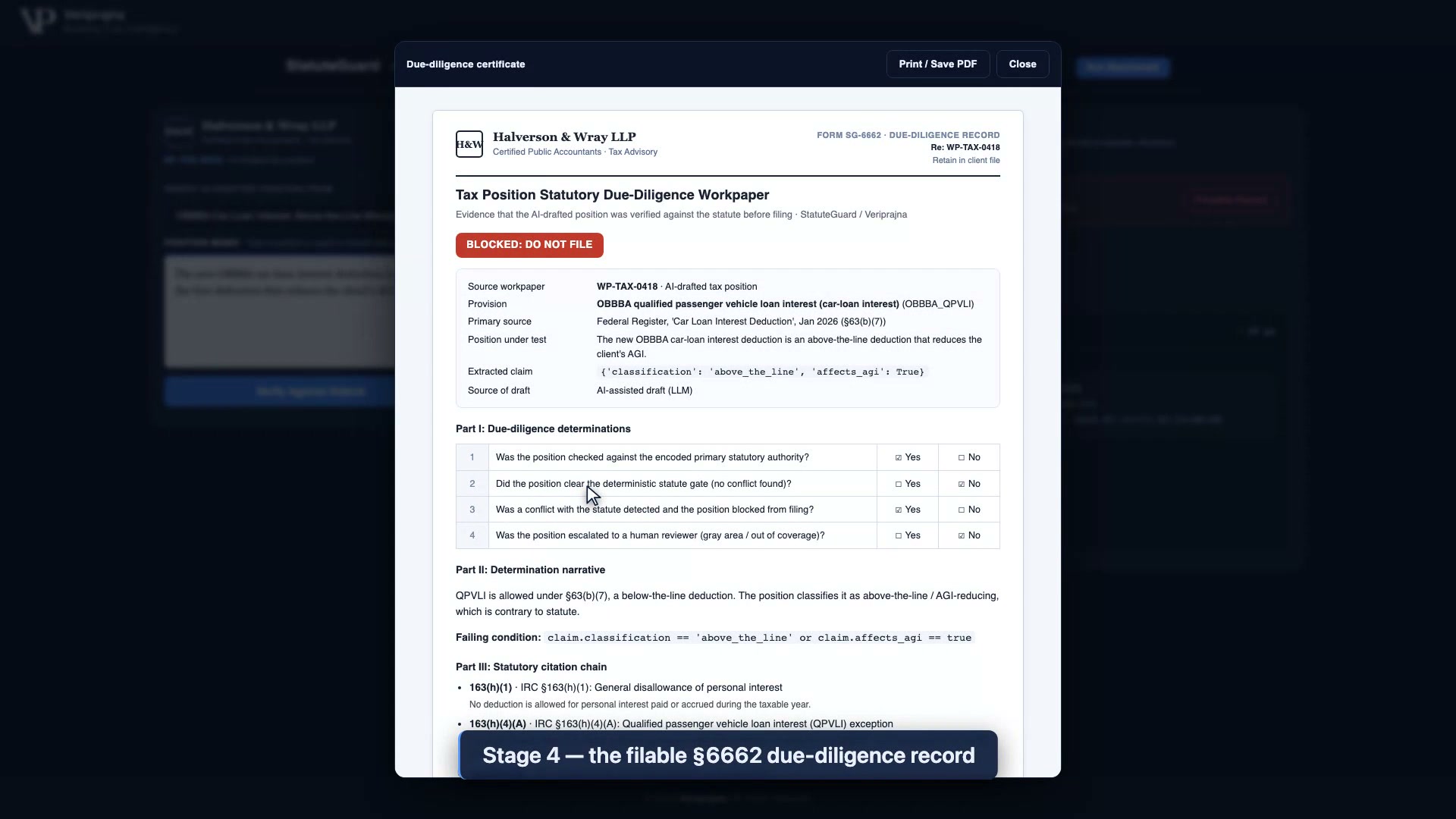

The anchor: an OBBBA car-loan-interest position drafted as above-the-line

A drafted statement reads: "The new OBBBA car-loan interest deduction is an above-the-line deduction that reduces the client's AGI." It is plausible, well written, and wrong. Qualified passenger vehicle loan interest is a below-the-line deduction under §63(b)(7); it does not reduce AGI. Per the demo's own README, mainstream tax-prep guidance (including H&R Block's site) has mislabeled it above-the-line. StatuteGuard returns BLOCK: DO NOT FILE, animates the citation chain §163(h)(1) → §163(h)(4)(A) → §63(b)(7) → §62/§63, and flags a 5-way downstream cascade of what breaks if filed as drafted: AGI, AGI-coupled state tax, Medicare IRMAA premiums, the medical-expense deduction floor, and student-loan income-driven repayment.

The extraction step took 5.93s; the deterministic grounding rendered its verdict in microseconds.

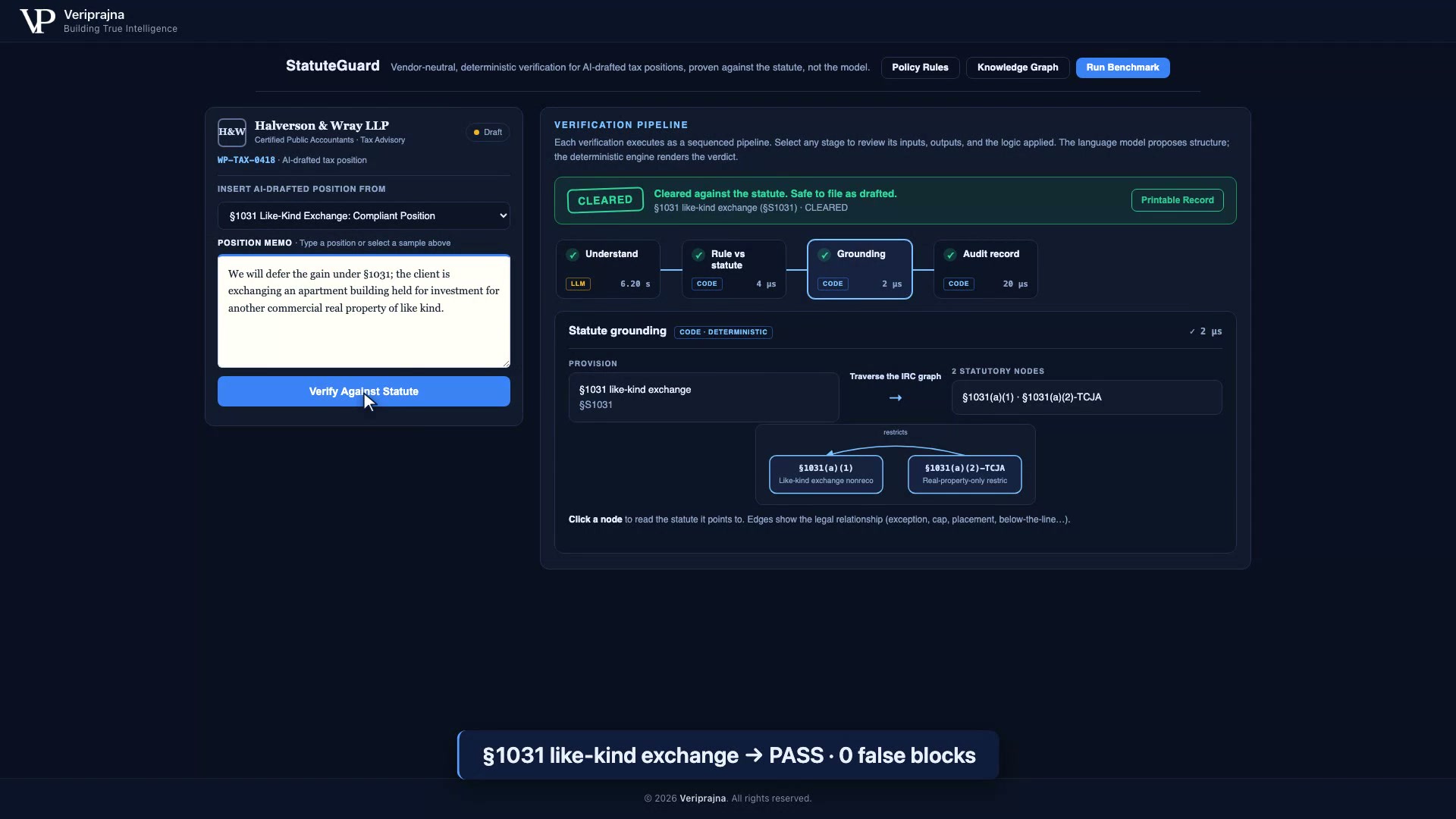

A clean §1031 exchange passes

A compliant like-kind exchange of investment real property returns CLEARED: safe to file as drafted, with its own two-node citation chain (§1031(a)(1) and §1031(a)(2)-TCJA). This is the discipline that matters: a correct position is never wrongly flagged. Gate precision is 100% with 0 false blocks on the golden set.

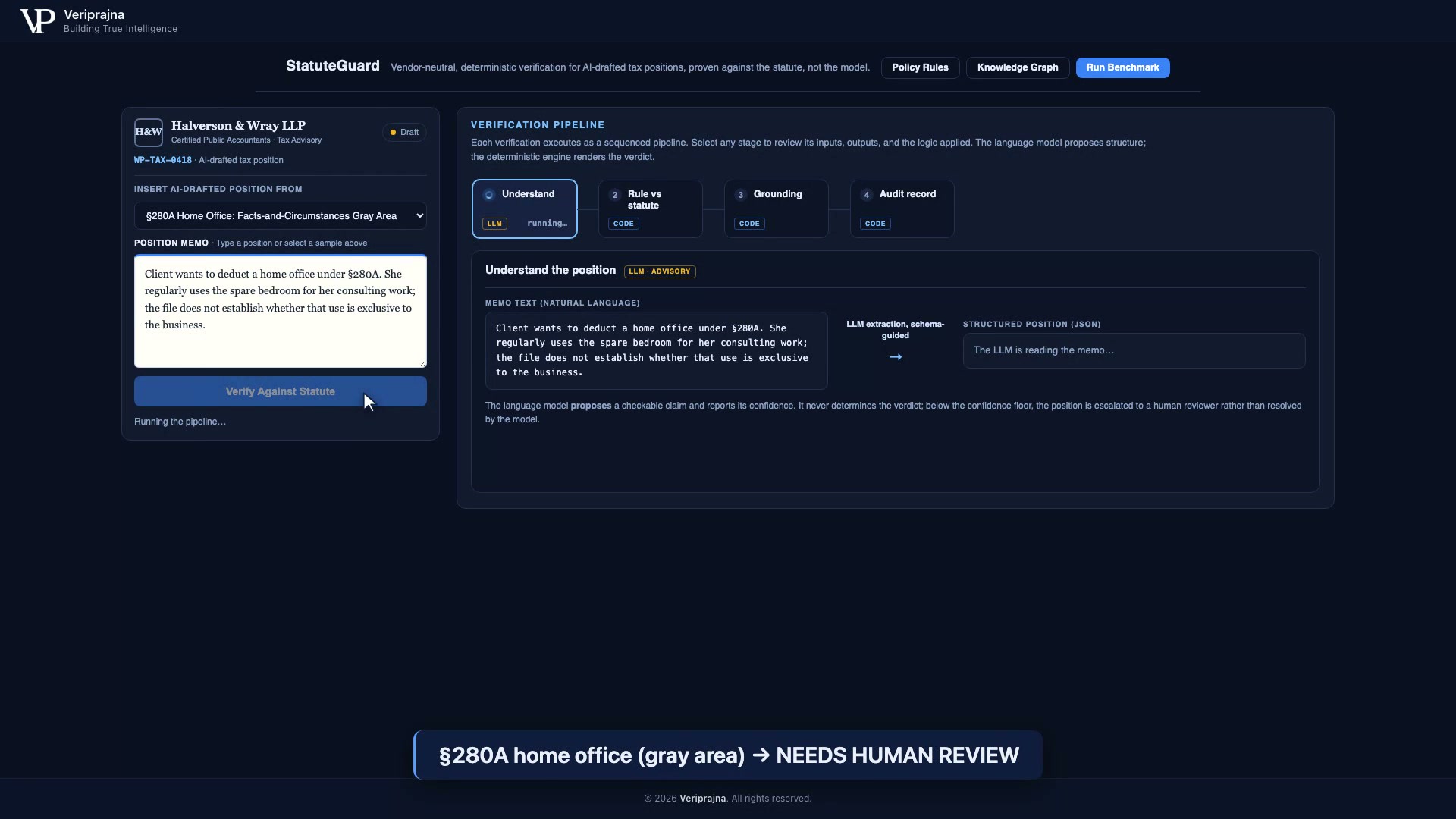

A §280A gray area escalates

A home-office position where the file does not establish exclusive business use is a facts-and-circumstances test, outside deterministic coverage. StatuteGuard returns NEEDS HUMAN REVIEW rather than bluffing. The LLM proposes a checkable claim and reports confidence; below the floor, the position is escalated, never resolved by the model.

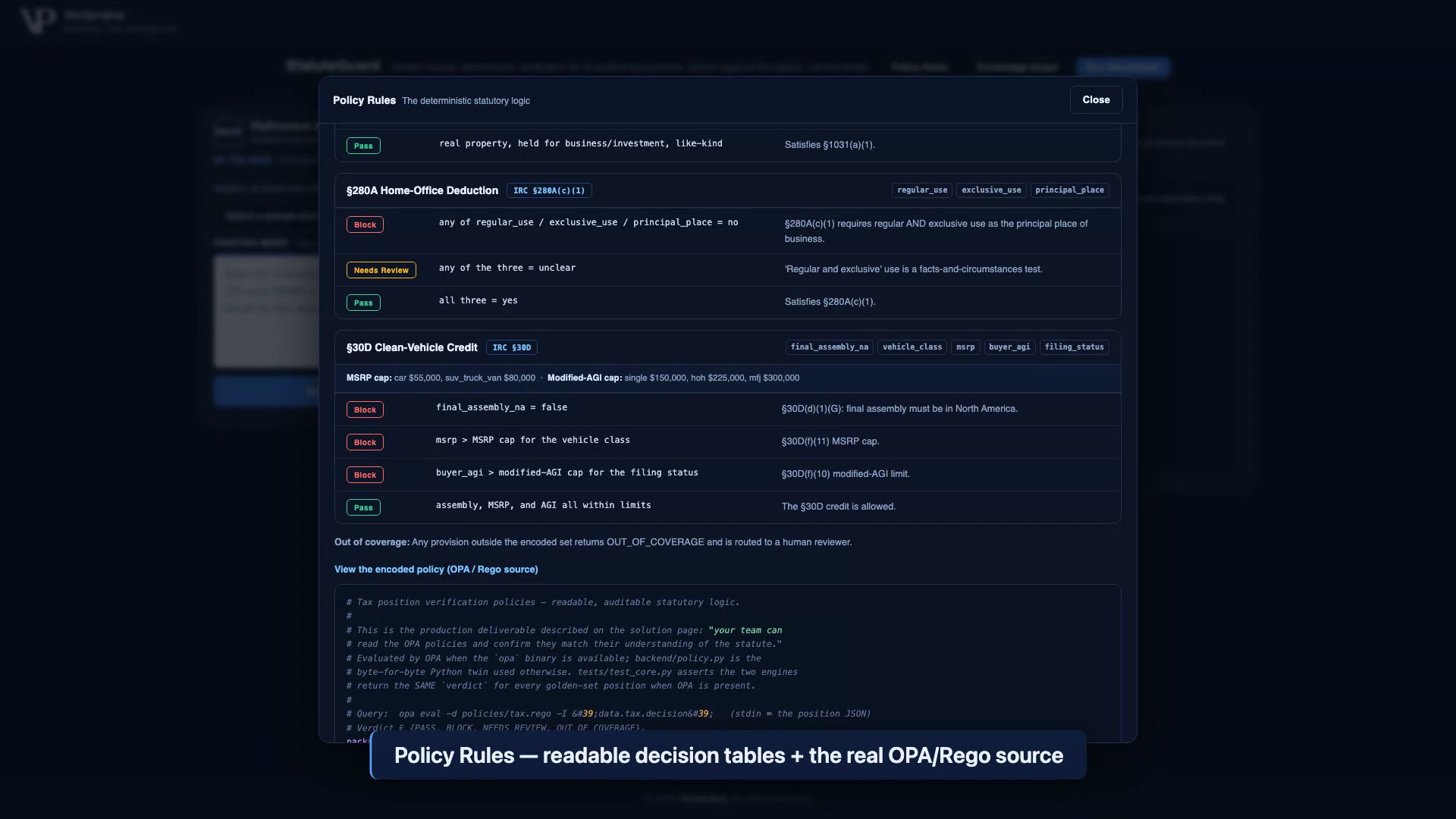

You can read the policies yourself

The Policy Rules viewer shows the deterministic statutory logic as readable decision tables next to the real OPA/Rego source. This is the point of a verification layer you can defend: you confirm the code matches the statute, rather than trusting a model's summary of it.

Every verdict writes a filable record

The audit stage produces a Form SG-6662 due-diligence workpaper: the source, the primary statutory authority, the extracted claim, the determination narrative, and the full citation chain, ready to print or save as PDF and retain in the client file. It supports a §6662 reasonable-cause position; it is not advice.

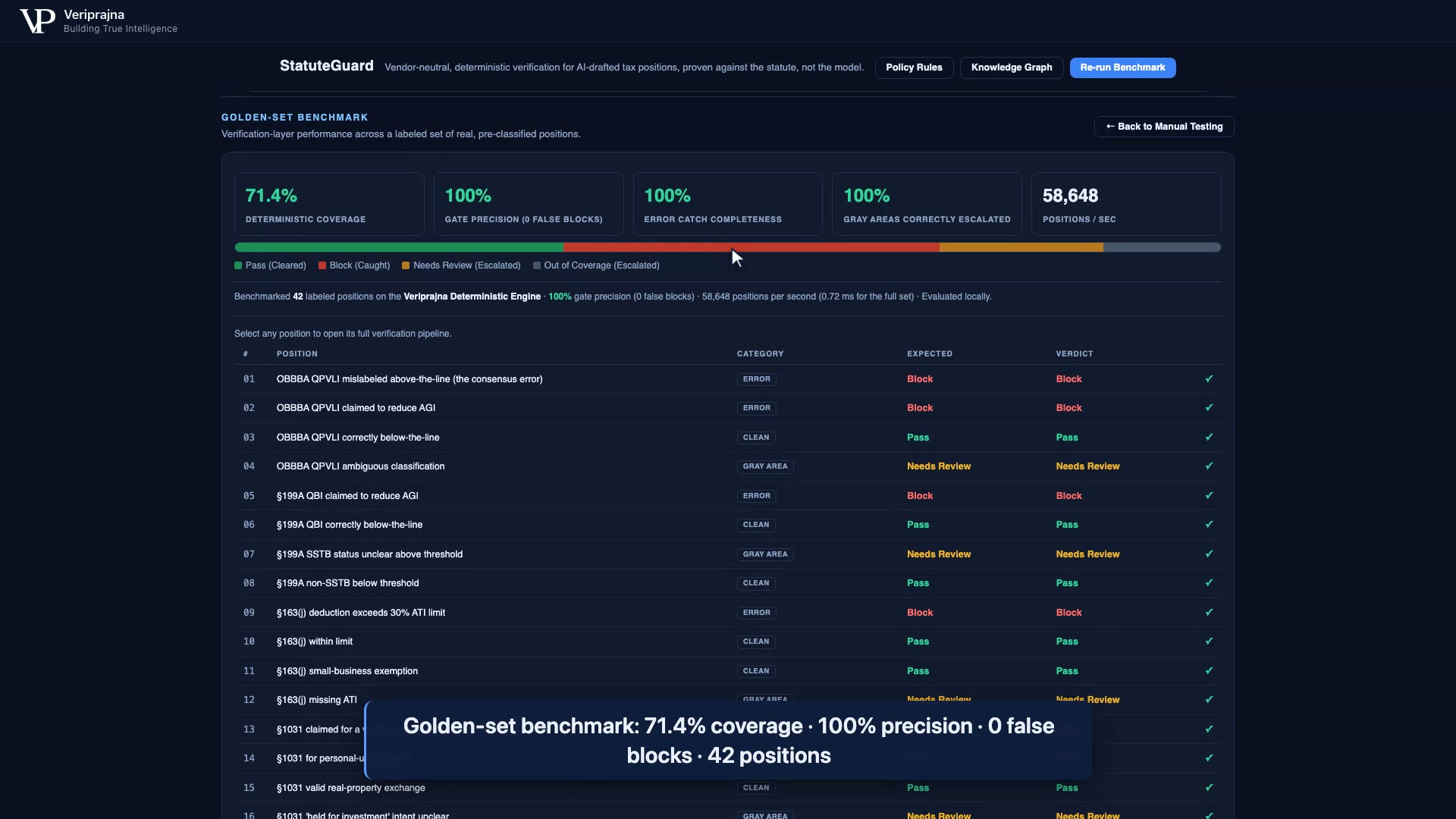

Measured on a labeled golden set, evaluated locally

Run Benchmark replays a 42-position labeled golden set (14 clean, 16 error, 12 escalate). The scoreboard reports 71.4% deterministic coverage, 100% gate precision with 0 false blocks, 100% error-catch completeness, and 100% correct escalation of gray areas, with every verdict matching its label. These describe the verification layer, not a model error rate, so they hold as base models improve. During the build the verdicts were cross-checked against OPA 1.17.1 and matched the pure-Python twin exactly on all 42 cases.

These numbers are measured on a fixed 42-case labeled golden set of the encoded provisions, not an open-world guarantee.